—US single-family rent prices increased 3.2 percent year over year in January 2019—

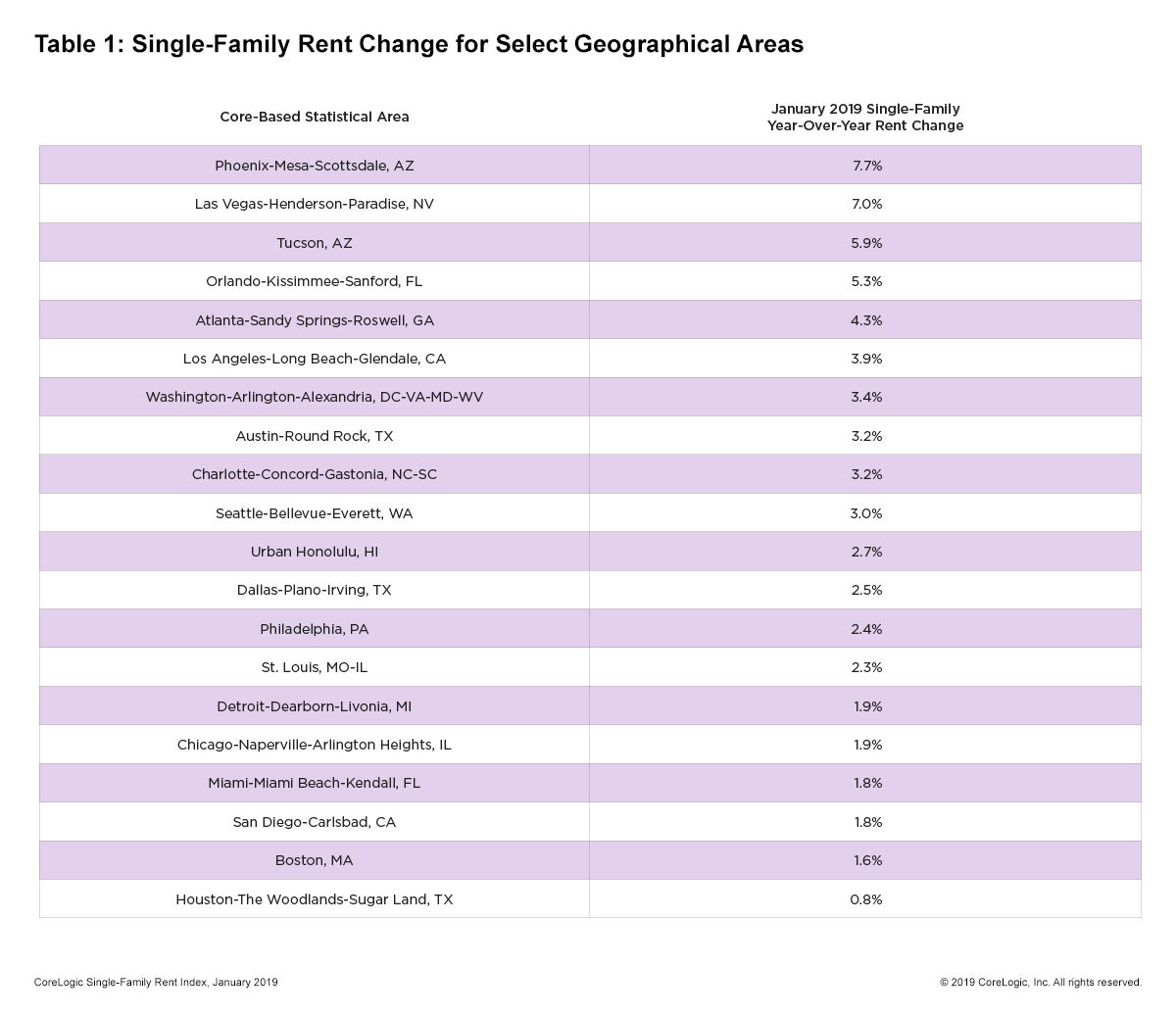

- Phoenix had the highest year-over-year rent price increase at 7.7 percent

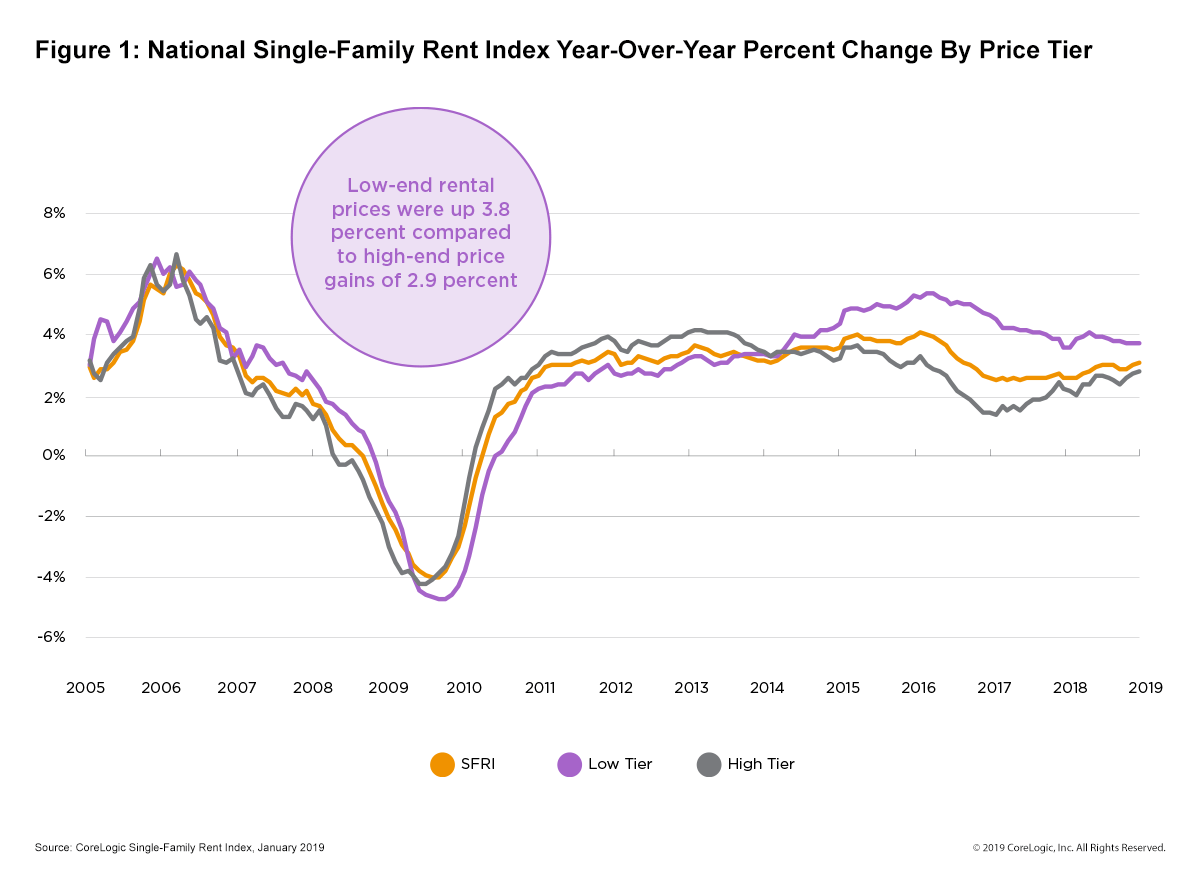

- Low-end rent prices were up 3.8 percent, compared to high-end price gains of 2.9 percent

- The U.S. rent price increase was the fastest since September 2016

CoreLogic® (NYSE: CLGX), a leading global property information, analytics and data-enabled solutions provider, today released its latest Single-Family Rent Index (SFRI), which analyzes single-family rent price changes nationally and among 20 metropolitan areas. Data collected for January 2019 shows a national rent increase of 3.2 percent, compared to 2.7 percent in January 2018.

Low rental home inventory, relative to demand, fuels the growth of single-family rent prices. The SFRI shows single-family rent prices have climbed between 2010 and 2019. However, overall year-over-year rent price increases have slowed since February 2016, when they peaked at 4.2 percent, and have stabilized over the last year with a monthly average of 3 percent.

National rent growth continued to be propped up by low-end rentals in January. Rent prices among this tier, defined as properties with rent prices less than 75 percent of the regional median, increased 3.8 percent year over year in January 2019, up slightly from the 3.7 percent increase experienced in January 2018. Meanwhile, high-end rentals, defined as properties with rent prices greater than 125 percent of a region’s median rent, increased 2.9 percent in January 2019, up from 2.4 percent in January 2018.

Among the 20 metro areas shown in Table 1, Phoenix had the highest year-over-year increase in single-family rents in January 2019 at 7.7 percent (compared to January 2018), followed by Las Vegas at 7 percent. Tucson, Arizona experienced the third highest year-over-year rent increase at 5.9 percent. This is the first time Tucson, Arizona was among the top three metros for rent growth in more than 12 months. Rent prices in disaster-affected areas like Houston saw steady growth throughout 2018. However, for the second consecutive month, Houston experienced the lowest rent increases of all analyzed metros at 0.8 percent. This is the lowest rent growth for the Houston metro area since September 2017 in the immediate aftermath of Hurricane Harvey.

Metro areas with limited new construction, low rental vacancies and strong local economies that attract new employees tend to have stronger rent growth. Phoenix and Orlando, Florida experienced high year-over-year rent growth in January, driven by employment growth of 3.1 percent and 3.9 percent year over year, respectively. This is compared with the national employment growth average of 2 percent, according to data from the United States Bureau of Labor Statistics.

“Rent prices for single-family homes increased 3.2 percent in January, which was the fastest increase in more than two years,” said Molly Boesel, principal economist at CoreLogic. “Demand for single-family rentals has remained brisk, and while employment growth has played a role in rental demand, demographics have as well. Households headed by someone under the age of 35 are more likely to rent than own, and with nearly a quarter of the U.S. population between the ages of 18 and 35, this age group continues to feed the demand for single-family rentals.”

Methodology

The single-family rental market accounts for half of the rental housing stock, yet unlike the multifamily market, which has many different sources of rent data, there are minimal quality adjusted single-family rent transaction data. The CoreLogic Single-Family Rent Index (SFRI) serves to fill that void by applying a repeat pairing methodology to single-family rental listing data in the Multiple Listing Service. CoreLogic constructed the SFRI for over 70 Core Based Statistical Areas (CBSAs)—including 40 CBSAs with four value tiers—and a national composite index.

Source: CoreLogic

The data provided is for use only by the primary recipient or the primary recipient’s publication or broadcast. This data may not be re-sold, republished or licensed to any other source, including publications and sources owned by the primary recipient’s parent company without prior written permission from CoreLogic. Any CoreLogic data used for publication or broadcast, in whole or in part, must be sourced as coming from CoreLogic, a data and analytics company. For use with broadcast or web content, the citation must directly accompany first reference of the data. If the data is illustrated with maps, charts, graphs or other visual elements, the CoreLogic logo must be included on screen or website. For questions, analysis or interpretation of the data, contact Alyson Austin at [email protected] or Allyse Sanchez at [email protected]. Data provided may not be modified without the prior written permission of CoreLogic. Do not use the data in any unlawful manner. This data is compiled from public records, contributory databases and proprietary analytics, and its accuracy is dependent upon these sources.

About CoreLogic

CoreLogic (NYSE: CLGX) is a leading global property information, analytics and data-enabled solutions provider. The company’s combined data from public, contributory and proprietary sources includes over 4.5 billion records spanning more than 50 years and providing detailed coverage of property, mortgages and other encumbrances, consumer credit, tenancy, location, hazard risk and related performance information. The markets CoreLogic serves include real estate and mortgage finance, insurance, capital markets, and the public sector. CoreLogic delivers value to clients through unique data, analytics, workflow technology, advisory and managed services. Clients rely on CoreLogic to help identify and manage growth opportunities, improve performance and mitigate risk. Headquartered in Irvine, Calif., CoreLogic operates in North America, Western Europe and Asia Pacific. For more information, please visit www.corelogic.com.

CORELOGIC and the CoreLogic logo are trademarks of CoreLogic, Inc. and/or its subsidiaries.