Defined Regions

CoreLogic® curates this monthly bulletin of regional construction cost insights, which are reflected in the CoreLogic Claims Pricing database. We combine the current month’s pricing data with four common loss scenarios to create models illustrating market impacts across nine regions, which are compared month over month and year over year.

Our experts provide detailed analyses of changes and trends to provide additional insight into key drivers. View our Construction Database Pricing Methodology whitepaper to gain additional insight into how we populate cost values.

September Pricing Insights

The midpoint of the 2023 hurricane season is approaching on Sept. 10, and so far, there has not been any generalized pricing movement across the regions that can be attributed to hurricane damage.

However, severe convective storms over the past two months have caused widespread damage to residences in Minnesota, Colorado, Virginia, Arizona, Maryland, North Carolina, and Wisconsin. Potential market pricing shifts are being monitored accordingly. Although labor and material combined pricing for roofing, siding, and windows have not shown any significant increases month over month, they remain elevated over 2022 pricing.

Report Highlights

Material

Material components can be characterized in one of two ways: Pricing that is significantly lower than in 2022 and pricing that is significantly higher than in 2022.

Lumber-based products, such as framing, fencing, cabinetry, and rough/finished carpentry, continue to be well below the pricing of a year ago. On the other hand, drywall, insulation, tile, paint, and window pricing all remain elevated. These differences will be discussed in further detail throughout the bulletin.

Labor

Most labor categories have settled in at levels 4.6% higher than September 2022. The exception is roofers, where the average cost is 9.3% higher across all regions. The steepest roofing wages are found in the Gulf Coast, Southeast, and Central regions, where rates were respectively 12.1%, 10.1%, and 9.9% higher than a year ago.

Fire/Lightning (Large Loss) Insights: 12-Month Trend

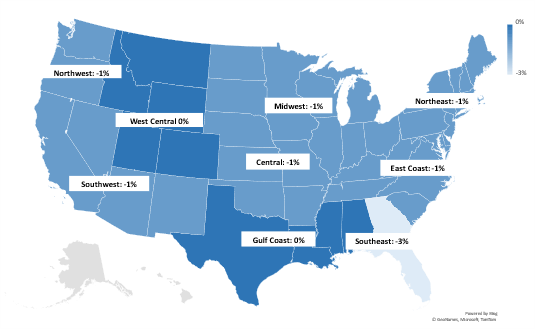

In this category, large loss claims are modeled from a typical fire loss where all components of a home’s construction are affected. Losses typically exceed $100,000.

- This loss scenario decreased in all regions by 0.6% or less. Year-over-year analysis shows the Gulf Coast and West-Central regions are on par with 2022 pricing, while the Southeast dropped by 3%. All remaining regions dropped by 1%. All regions remain above Q1 2022 levels.

- Overall, continued stability of the labor component for September contributed to minimal monthly change for this loss scenario. Conversely, labor rates are elevated compared to last year and contribute to the inflation of the overall loss scenario.

- Here’s a closer look at the high/low material pricing for the Southeast, as it is the only region with significant changes compared to 2022.

| Significant Southeast Material Price Changes Since 2022 | |

| Framing/Rough Carpentry | -40.8% |

| Finish Carpentry | -10.9% |

| Cabinetry | – 8% |

| Drywall | 16.3% |

| Insulation | 5.9% |

| Tile | 7.8% |

Wind/Hail (Exterior/Roof) Insights: 12-Month Trend

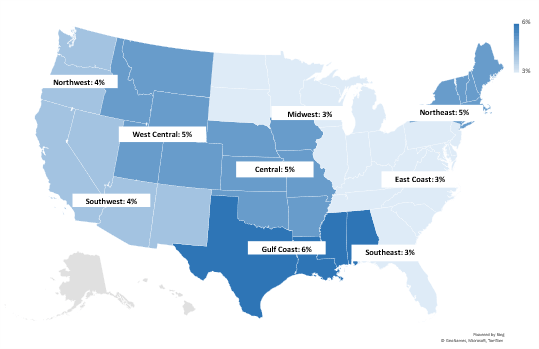

This category represents losses due to wind and/or hail weather activity. Restoration from this damage requires roof replacement, partial siding replacement, and accompanying accessories.

- CoreLogic Weather Verification Services, monitored and recorded events with 1-inch or greater hail from July 30 through Aug. 25 of this year. A total of 35 states and 762,500 homes were affected with the most severe damage occurring in Minnesota and Colorado. In the Minnesota counties of Hennepin and Ramsey, 193,000 homes were impacted by 1-inch or greater hail on Aug. 11. In Colorado’s El Paso County, storms occurring on July 31 and August 5 struck 125,000 homes with 1-inch or greater hail.

- Across all regions, this loss scenario remains elevated, averaging 4.2% higher than last year. The Gulf Coast, Central, Northeast, and West-Central regions are nearly 1% higher than this average. With continued natural catastrophe events in these regions, the CoreLogic Pricing Data team will assess post-loss amplification factors to determine if pricing adjustments are warranted.

- Of the housing components that are most likely to be damaged in a wind/hail event, window pricing remains the highest at 5.7% above last year. Not surprisingly, many of the hardest-hit regions with large wind/hail events maintained elevated year-over-year window pricing. Prices rose in the Central U.S. by 8.4%, on the Gulf Coast they increased by 9.4%, on the West Coast they jumped 11.7%, and in the Northeast they climbed 5.7%.

Water (Interior Reconstruction) Insights: 12-Month Trend

Moderately complex losses are modeled for the interior water loss scenario using the bathroom as the origin of loss where a combination of replacement and repair of common household finishes is required.

- Very little movement occurred in the pricing for the water (interior reconstruction) scenario, with less than -0.3% decline across all regions. After last month’s drop in the year-over-year comparison, pricing has leveled out at 3.6% on average across all regions.

- For September, the two biggest material movers are drywall and framing/rough carpentry. After a slight dip in pricing last month, drywall is experiencing a 1.7% average increase across all regions, while framing/rough carpentry continues to drop in price by 4.6% this month.

- Labor averages for this loss scenario experienced no major changes in September. As expected, with year-over-year interior reconstruction pricing leveling out, labor rates have remained steady at 4.6% higher than last year.

Water Mitigation (Drying) Insights: 12-Month Trend

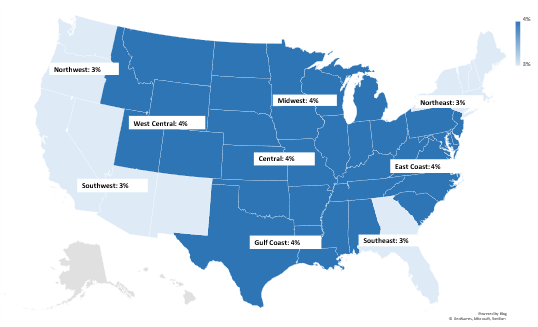

Typical drying costs for a residential structure include water extraction, wet material removal, and drying equipment use.

- The water mitigation scenario continues a three-month trend with very little movement month over month. In September, there was a slight decrease of less than 0.03% across all regions.

- No increase in labor rates occurred for water remediation technicians this month. However, compared to September 2022, water remediation technician rates are, on average, 4.7% higher, with the Northwest region seeing labor rates 5.8% higher than this time last year.

- All regions surpassed September 2022 pricing for this loss scenario, with two regions far exceeding the average.

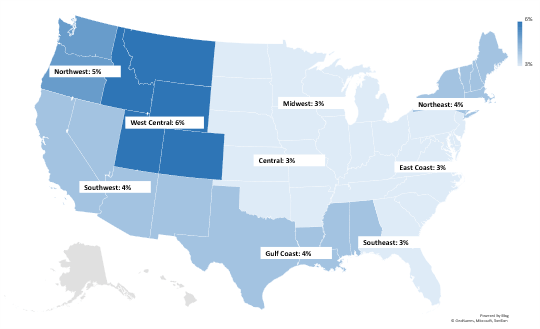

| Average Increase Versus 2022 Pricing (All Regions) | 3.9% |

| Northwest Region | 5% |

| West-Central Region | 6% |

About CoreLogic Data Research

CoreLogic develops this report using up-to-date materials and labor costs. CoreLogic’s team of analysts continuously researches hard costs such as labor, material, and equipment, including mark-ups. CoreLogic updates its database every month accordingly.

Our research also covers soft costs such as taxes and fringe benefits for reconstruction work performed as part of the insurance industry. CoreLogic monitors demographics and econometric statistics, government indicators, and localization requirements, including market trends from thousands of unique economies throughout the United States.

Other factors in this process include the following:

- Wage rates for more than 85 union and non-union trades

- Over 100,000 construction data points

- Productivity rates and crew sizes

- Building code requirements and localized cost variables

Additionally, we validate cost data by analyzing field inspection records, contractor estimates, phone surveys, and both partial and complete loss claim information.

Please complete the online form to provide feedback or request information on any items in our construction database. Please contact your sales executive or account manager for additional explanations or questions. A more detailed methodology explanation can be found in our Construction Database Pricing Methodology whitepaper.

About CoreLogic

CoreLogic is a leading global property information, analytics and data-enabled solutions provider. The company’s combined data from public, contributory and proprietary sources includes over 4.5 billion records spanning more than 50 years, providing detailed coverage of property, mortgages and other encumbrances, consumer credit, tenancy, location, hazard risk and related performance information. The markets CoreLogic serves include real estate and mortgage finance, insurance, capital markets, and the public sector. CoreLogic delivers value to clients through unique data, analytics, workflow technology, advisory and managed services. Clients rely on CoreLogic to help identify and manage growth opportunities, improve performance and mitigate risk. Headquartered in Irvine, Calif., CoreLogic operates in North America, Western Europe and Asia Pacific. For more information, please visit www.corelogic.com.

NOTE: The building material, labor, and other cost information in this bulletin is generated using research, sources, and methods current as of the date of this bulletin and is intended only to provide an estimated average of reconstruction cost trends in the specified general geographic regions of the United States. This cost information may vary further when adjusting claim values for specific property locations or specific business conditions.